Google Cloud revenue jumped 48% year over year, now accounting for 15.5% of Alphabet’s total sales.

Analyst growth estimates may be too conservative given Alphabet’s history of accelerating earnings growth.

The stock trades at 24 times forward earnings with a PEG ratio of 2.0; not exactly cheap but also not extreme for a tech giant with AI momentum.

Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL) reported Q4 2025 results last Tuesday. Google’s parent company eclipsed Wall Street’s estimates across the board, with a 2.4% revenue surprise and 6.8% outperformance on the bottom line.

Image source: Alphabet.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

Google Cloud was the star of the show. Sales rose 48% year over year to $17.7 billion, accounting for a beefy 15.5% of Alphabet’s total revenues. The segment’s operating income also soared, rising 154% to $5.3 billion.

These results show how Alphabet taps into the artificial intelligence (AI) boom. However, the stock took a dive after the report as investors focused on Alphabet’s enormous AI infrastructure spending plans.

Was the price drop appropriate, or is Alphabet the best AI stock to buy right now? Let’s take a look.

As of Feb. 6, Alphabet’s stock has fallen 6.5% since the Q4 report. The stock is trading at prices not seen since Jan. 20, also known as “a couple of weeks ago.” So, it’s not a massive price cut, but still a deep enough drop to raise eyebrows. With a $3.9 trillion market cap, Alphabet lost about $250 billion of market value in three days.

When giants stumble, Wall Street shakes. However, Alphabet remains the best performer among the “Magnificent Seven” stocks over the last year. The stock has gained 68%, far ahead of Nvidia‘s (NASDAQ: NVDA) runner-up jump of 47%.

You can look at Alphabet’s valuation from several angles.

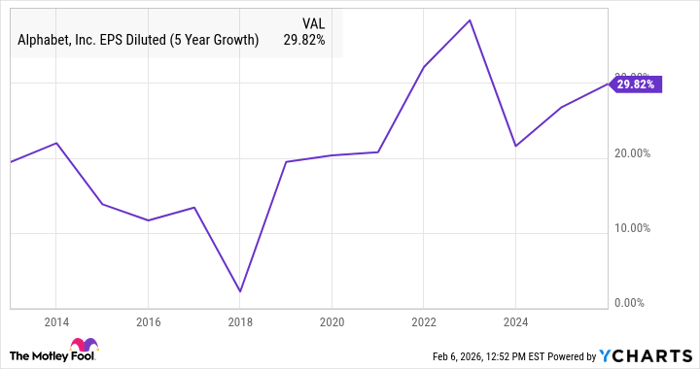

Alphabet has a history of accelerating its bottom-line growth over time, though:

GOOGL EPS Diluted (5 Year Growth) data by YCharts. EPS = earnings per share.

Google Cloud has a lot of growing left to do, which is why Alphabet is doubling its capital expense budget in 2026 in the first place. And this fast-growing business segment’s operating margin nearly doubled over the last year, from 17.5% to 29.9%.

I can’t guarantee that Alphabet’s stock will beat the other Magnificent Seven tickers in 2026 or over the next three years. But I’m convinced that the analyst community should give Alphabet’s growth prospects more credit.

So, yes, I think Alphabet belongs at the top of any serious AI stock watch list. The company has spent two decades turning data into dollars, and Google Cloud is the latest proof that the playbook still works. Growth investors get a cloud business that’s just hitting its stride; long-term holders get a company that knows how to evolve.

That’s a combination I’m happy to buy at Alphabet’s current valuation.

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $443,299!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,136,601!*

Now, it’s worth noting Stock Advisor’s total average return is 914% — a market-crushing outperformance compared to 195% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 8, 2026.

Anders Bylund has positions in Alphabet and Nvidia. The Motley Fool has positions in and recommends Alphabet and Nvidia. The Motley Fool has a disclosure policy.

—

Blog powered by G6

Disclaimer! A guest author has made this post. G6 has not checked the post. its content and attachments and under no circumstances will G6 be held responsible or liable in any way for any claims, damages, losses, expenses, costs or liabilities whatsoever (including, without limitation, any direct or indirect damages for loss of profits, business interruption or loss of information) resulting or arising directly or indirectly from your use of or inability to use this website or any websites linked to it, or from your reliance on the information and material on this website, even if the G6 has been advised of the possibility of such damages in advance.

For any inquiries, please contact [email protected]