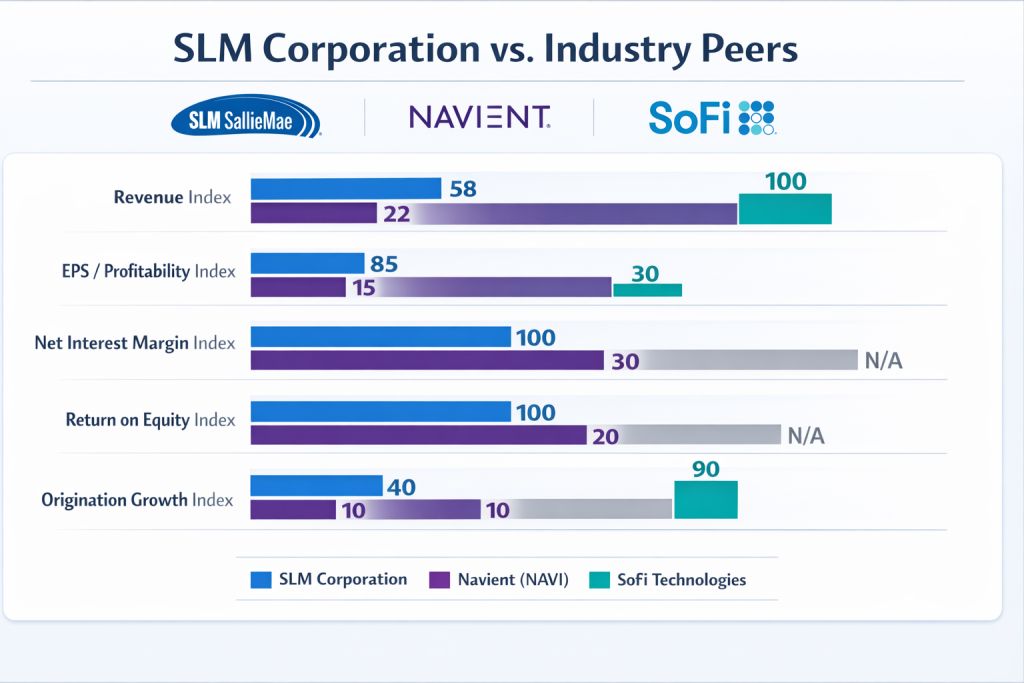

SLM Corporation Dominance and Strategic Transformation

SLM Corporation (Sallie Mae) is the preeminent leader in the private education loan (PEL) space, holding an estimated 60% to 67% market share in undergraduate and graduate originations. The company delivered a robust performance in 2025, reporting GAAP diluted earnings per share of $3.46, a 29% increase over the previous year. Its dominance is underpinned by a massive footprint of 2,400 active university relationships and a highly disciplined underwriting model, with an average FICO score of 755 at approval.

Sallie Mae is currently undergoing a strategic shift toward a “capital-light” model, exemplified by a November 2025 partnership with KKR to sell over $6 billion in loans over three years while retaining the servicing rights to generate recurring fee income. This transformation aims to mitigate sensitivity to interest rate fluctuations and rising funding costs, which compressed its Net Interest Margin (NIM) to 5.18% by the end of 2025.

American Student Lending Market

The American student lending market is a complex ecosystem dominated by the federal government, but it also features a robust segment of private financial institutions and third-party service providers. As of late 2024, approximately 93% of all U.S. student debt is owned by the federal government, representing a massive shift from 2010 when that figure was only 55%.

SLM Corporation (Sallie Mae) stands as the dominant leader in the private student loan sector, holding an estimated 60% to 67% market share in undergraduate and graduate originations. Its position was further strengthened by the exit of major competitors like Discover from the space.

Key Competitors and Market Performance

The following are the key categories and players currently operating in the market:

The Dominant Lender: Federal Student Aid (FSA)

The U.S. Department of Education, through its principal office Federal Student Aid (FSA), is the largest provider of student financial assistance in the United States. FSA is a Performance-Based Organization (PBO) responsible for implementing programs authorized under the Higher Education Act of 1965. As of the end of fiscal year 2024, FSA manages an outstanding federal student loan portfolio of more than $1.6 trillion belonging to approximately 45 million borrowers.

Federal Loan Servicers

While the government owns the loans, it contracts with private companies to handle the day-to-day administration, billing, and customer service for federal borrowers. Under the Unified Servicing and Data Solution (USDS), the primary contracted servicers are:

Nelnet: One of the largest servicers, managing over $526 billion for 15.5 million borrowers.

Aidvantage: A subsidiary of Maximus Education, which took over Navient’s federal loan portfolio in late 2021.

MOHELA (Missouri Higher Education Loan Authority): A major servicer that previously managed the Public Service Loan Forgiveness (PSLF) program as an interim specialty servicer.

EdFinancial: A mid-level servicer that was recently awarded a new federal contract in 2024.

Central Research, Inc. (CRI): A veteran-owned company and the newest entrant to the federal loan servicing space.

Private Lenders and Financial Institutions

Private student loans are issued by financial institutions and are based on the creditworthiness of the borrower or a co-signer. The most significant private players include:

Sallie Mae (SLM Corporation): Historically the most influential player in the industry, it transitioned from a government-sponsored entity to a fully private corporation and remains a leader in loan origination and private lending.

SoFi Technologies: A prominent fintech lender that specializes in student loan refinancing and has seen rapid growth in originations.

Discover Financial Services: A major owner of private debt, though its portfolio was recently involved in a massive $35.3 billion acquisition by Capital One.

Navient: Formerly a federal servicer, Navient remains one of the largest owners and lenders of private student debt.

Citizens Bank: Identified as one of the major industry leaders in the student loan market.

Specialized and Legacy Participants

National Collegiate Student Loan Trusts (NCT): One of the nation’s largest owners of securitized private student debt, often involving student loan asset-backed securities (SLABS).

Guaranty Agencies (GAs): These state or nonprofit agencies (such as USA Funds) historically insured lenders against losses from defaulted loans in the legacy Federal Family Education Loan (FFEL) program. While no new FFEL loans have been made since 2010, GAs still monitor compliance and service their defaulted loan portfolios.

Private Collection Agencies (PCAs): These third-party entities are contracted to recover funds from defaulted loans.

Current Scenario and Financial Standings

Strong Earnings: Sallie Mae closed 2025 with robust performance, reporting GAAP diluted earnings per share of $3.46, a 29% increase over 2024.

Strategic Evolution: The company is transitioning to a “capital-light” model, emphasizing strategic partnerships and loan sales. A key example is its 2025 agreement with KKR to sell over $6 billion in loans over three years while retaining the servicing rights to generate recurring fee income.

Credit Quality and Risks: While 96% of its loans in repayment were current at the end of 2025, the company faces rising headwinds from a 4.0% delinquency rate and increasing provisions for credit losses.

2026 Outlook

The scenario for SLM in 2026 remains positive but volatile. The company expects origination growth of 12% to 14% year-over-year. However, it must navigate a compressing Net Interest Margin (NIM), as rising funding costs for deposits begin to catch up with loan yields. While SLM is well-positioned to capture the volume shifted by federal PLUS reforms, it remains sensitive to macroeconomic factors like unemployment that could impact borrower repayment abilities.

Disclaimer! A guest author has made this post. G6 has not checked the post. its content and attachments and under no circumstances will G6 be held responsible or liable in any way for any claims, damages, losses, expenses, costs or liabilities whatsoever (including, without limitation, any direct or indirect damages for loss of profits, business interruption or loss of information) resulting or arising directly or indirectly from your use of or inability to use this website or any websites linked to it, or from your reliance on the information and material on this website, even if the G6 has been advised of the possibility of such damages in advance.